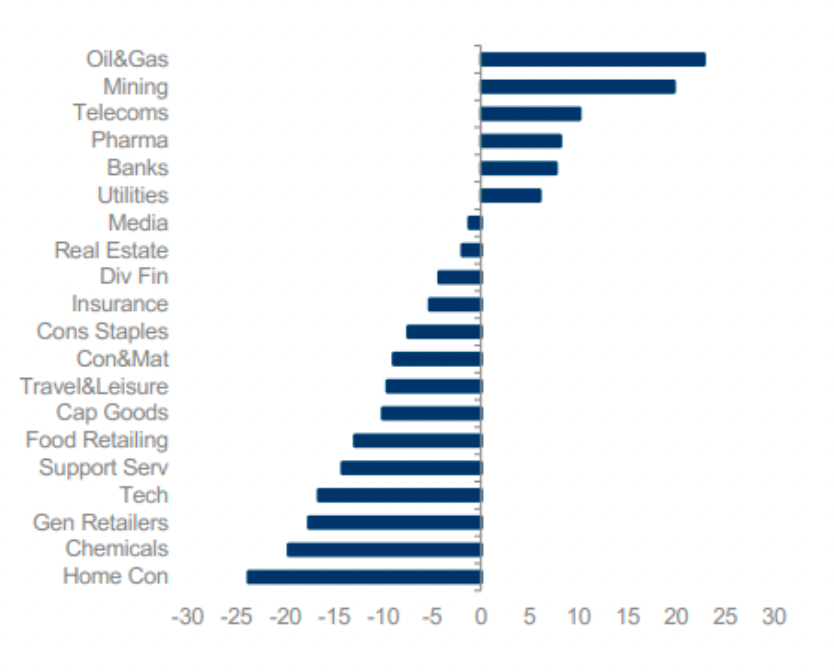

It’s been a volatile start to 2022, with the conflict in Ukraine creating huge disruption in oil markets, and adding to ongoing pressures seen in markets already dealing with the ongoing Covid-19 situation and supply chain issues. As such, Q1 22 has seen narrow markets led by commodities and mining (Figure 1)

Figure 1: Q1 relative performance (%)

Source: Morgan Stanley, March 2022

“There is nothing quite as seductive as vertical movements in price. They are the lanterns that draw every last moth”– Peter Atwater, author and speaker, University of Delaware

Regular readers will know, however, that we have long believed the UK is about much more than just commodities (and banks) – which differentiates us from the majority of our peers. We harbour deep reservations over the unforecastable nature of commodity prices and don’t feel we have an edge as active managers. We believe oil shares are often traded on a “mark-to-market”

basis, and that company managements have little visibility of future behaviour – affording investors limited scope to forecast or predict movement of stocks.

Additionally, the volatile nature of commodities is a concern in this rotational market. In 2008, for example, the oil price at the start of the year was around $95, rising to $150 in summer before ending the year on $50. Furthermore, in the long run we believe oil ultimately leads to deflation, offering only a temporary reprieve from inflation. As Ben Bernanke said in his 1997 paper Systematic Monetary Policy and the Effects of Oil Price Shocks1, “every oil shock has been deflationary not inflationary … as central banks mistake them for inflation and compound the tightening”. Admittedly, it felt painful not owning much oil and miners in H1 2008, but we felt much better about it in H2! We also feel most companies in the sector have poor returns on capital employed (ROCE) alongside heavy capex and debt burdens.

On the Columbia Threadneedle UK equities team we instead look to generate alpha through bottom-up stock analysis in areas we believe we do have a genuine edge. For example, the industrial sector, where the multiple levers affecting these businesses lend themselves far better to proper fundamental analysis.

Ultimately, then, although energy and materials mega-caps form a large proportion of the FTSE All Share index, we see a multitude of better opportunities for truly active managers to pursue risk-adjusted returns elsewhere and believe we have an edge in other sectors.

Oil price spike

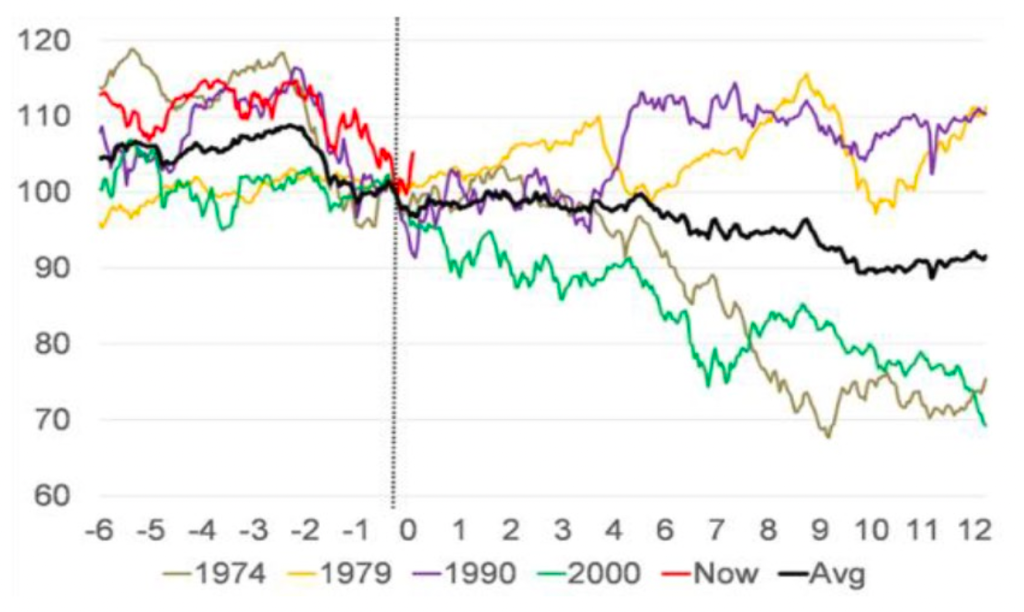

We would note, however, that every oil price shock is different. We can identify four events which look similar to today – ie Brent prices breaking through 2x its three-year moving average – but sometimes this marks a peak in prices (1990, 2000), and other times oil keeps rising (1979, 2000). After each of these shocks the US ISM Purchasing Managers Index (PMI) has fallen, indicating economic contraction. By contrast, the current US ISM value suggests strong momentum, which should help limit the damage. In terms of equity returns following an oil shock, the MSCI World Index fell 30% in the 12 months following the 1974 and 2000 oil peaks. But it was up 10% in the 12 months after those in 1979 and 1990 (Figure 2). So not always bad for equities!

Figure 2: MSCI AC World performance, six months before/12 months after oil spike

Source: Citi Research, March 2022

Mining – not an inflation hedge ultimately!

Mining, meanwhile, has outperformed the wider market by 20% over the past three months, but as a consequence the sector has become overbought and has risen above its 12-month average.2 This has once more been driven by mark-to-market earnings-per-share upgrades tracking the spike in commodity prices.

While metal markets may offer some short-term protection against inflation, the truth is prices – and therefore demand – are sensitive to the start of a substantial and sustained shift in the US Federal Reserve’s monetary policy. The Fed’s tightening will boost real rates, in turn elevating the opportunity cost of no-yield commodities versus the rising yields of other US dollar assets. Investors are likely to then reduce their exposure to commodity markets, regardless of any fundamental support that may exist in them. As Warren Buffet noted in his 1983 Annual Report, “the earnings of commodity businesses declined significantly in real terms during the 1970s, despite rampant inflation. The positive impact of rising sales is quickly offset by escalating spend on costs, capex and acquisitions to replace depleting resource bases.”3

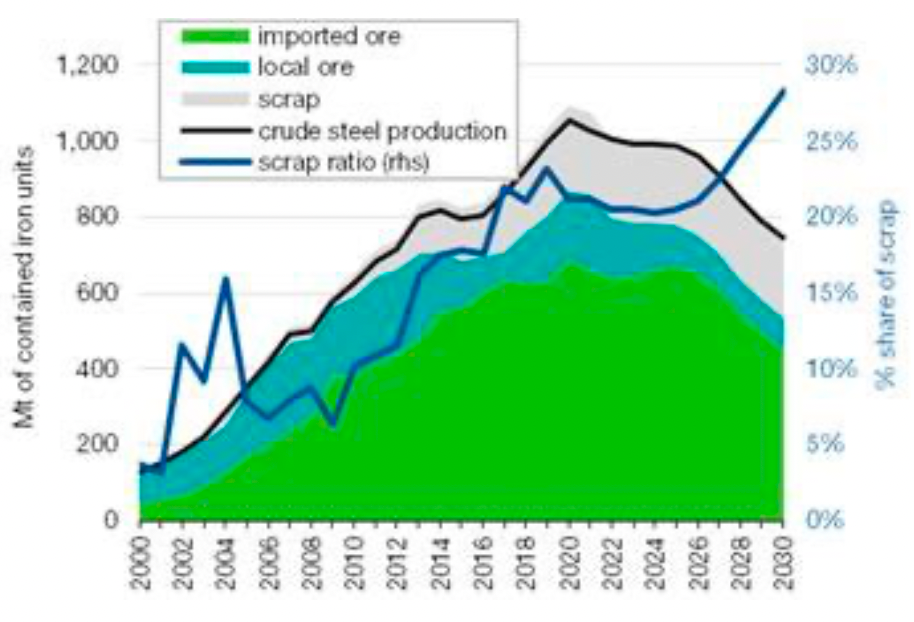

Separately, it is worth noting that the big demand driver for miners over the past 20 years has been China, and its construction boom days are behind us. In addition, the growing availability and use of scrap by the steel industry could come to represent a significant headwind to iron ore demand growth (Figure 3). With China also looking to go greener, it should offset any of US President Joe Biden’s infrastructure spending.

Figure 3: iron ore consumption falls in China

Source: Liberum, March 2022

All in all, we don’t believe this is the start of a super cycle; instead, it is a post-recession reflation trade created by a credit surplus and a global restocking, with the supply side being slow to respond. These typically last 12-18 months.

Cost of living pressure

The war in Ukraine has prompted a sharp de-risking in European banks and other cyclical sectors such as autos, travel and leisure, and industrials. If the conflict turns more constructive and the recessionary scenario of Europe recedes, we expect to see potential for money to come back to the space. The list of underperformers is littered with companies who suffered materially during Covid. Why are they seeing continuing share price weakness when their fundamental outlook is much stronger than 2020? We think this is quant driven, ie basket-trading machines that “shoot first and ask questions later”. Historic volatility is a key input for many systematic strategies, but a deep flaw is that it is necessarily backward looking and the two-year beta – or in other words sensitivity to market movements over the past two years – is heavily skewed by Covid volatility. So quality companies are being hit despite being better placed now than when the pandemic hit

Despite consumer confidence falling – unsurprisingly with the present uncertainties – there actually remains plenty to be optimistic about:

- Consumers have paid down their credit cards and balances as a percentage of GDP are below the long-run average

- Savings across the spectrum are higher than pre-pandemic

- We are at full employment and wages are growing, particularly at lower income levels.

Echoes of the Arab Spring

In 2011, the European/Greece crisis and the Arab Spring arrived as ripple effects from the aftermath of the 2008-09 global financial crisis. The current geopolitical turmoil could be seen as a rerun of this, stemming directly from the impact of the super loose monetary policy seen in the aftermath of Covid. We think the “flash crash” nature of March 2020’s downturn was slightly too quick and easy, and that there were always going to be bigger problems developing in global supply chains and distant economies. We would do well to remember that supply constraints and the cost-of-living squeeze are much more acute in some emerging markets (EMs).

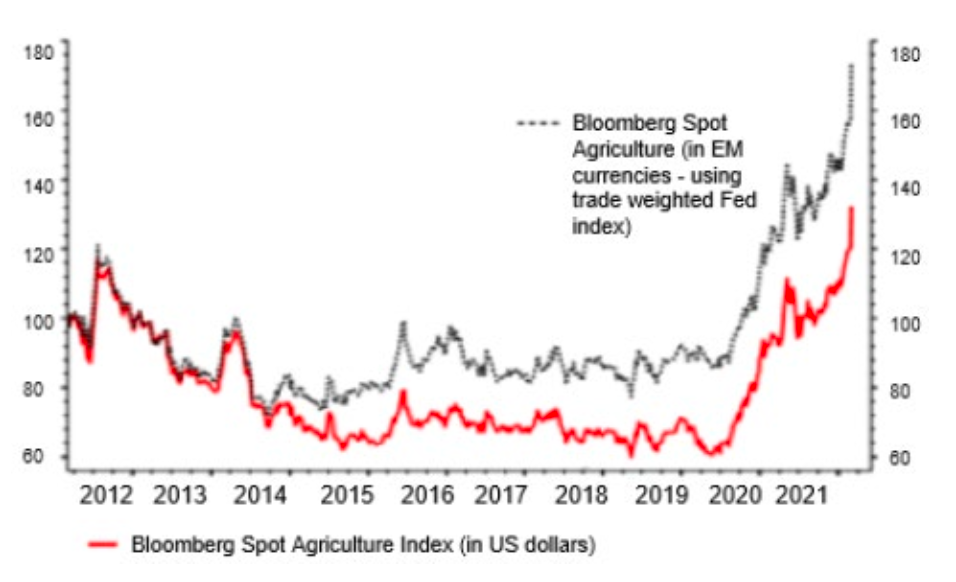

Indeed, it is not only energy prices that are spiking. World food prices jumped 24% year-on-year to record highs in February, led by vegetable oils and dairy products4, surpassing the Arab Spring high of 2011. The Bloomberg Agriculture spot price has risen a third over the past decade (Figure 4), but in EM terms the rise is more likely 75%.

Figure 4: food commodity price

Source: Albert Edwards SocGen, 4 March 2022

All the above feeds into polarised market opinions around the global economic outlook. Despite the recent rally heeding Nathan Rothschild’s famous 1810 adage “buy on the sound of cannons…”, recession looms front and centre in the pessimistic camp. The aforementioned worries over energy and food price shocks are largely to blame and reflected in dented consumer confidence as the knock to real incomes turns from headlines into reality. Together with close monitoring of the yield curve, the Fed tightening and a land war in Europe, it is unsurprising that fears of a cyclical bear market abound.

In the contrary camp, strong Western balance sheets coupled with high levels of savings and good ongoing levels of liquidity, as well as strong wealth effects supported by robust house prices and further fiscal spending in Europe in 2022, all point to a healthy and appealing equity market.

2022 – reasons to be cheerful!

As JP Morgan’s chief markets strategist said in November 2021, “the majority of equity investors don’t buy or sell shares based on stock-specific fundamentals”5. In fact, the US long-only fundamental active share of equity volumes is only 12%. With the rise in quant trading and ETF baskets driving markets, we would caution everyone to beware of whiplash. Although we’re seeing very rotational markets as a result of this basket trading, as fund managers we are not timing market moves. To paraphrase investor Charlie Munger, “we pick businesses … we are not stock jockeys!”.

Importantly, the opportunities for M&A within the UK persist, and inbound activity remains at record highs. The huge valuation arbitrage is continuing to stoke interest from private equity and foreign investors. In 2021 the UK saw 12 transactions in excess of $500 million – the most since 2007! Despite the conflict in Ukraine there will be more of this to come. Pearson6, for example, received its second and third bids while Putin was waging war. Although ultimately a deal was not agreed, interest has not peaked and UK-quoted assets continue to attract a lot of interest.

This is alongside recent take-outs of the likes of Morrisons, RSA and Cobham. We had large stakes in all of these and operated as genuine owners, engaging with company management teams and implementing positive change. This is integral to our philosophy and the stewardship approach we take to the companies we own. The bottom line is that there is still lots of dry powder out there, and we fully expect it will keep targeting the UK equity market.

So, all in all, the UK market remains a reliable alternative to highly valued, crowded trades. The proliferation of passive and quantitative-driven investing over the past few years, along with the recent volatility, has opened up opportunities for us as stock pickers and owners of businesses. As patient, conviction investors we will continue to avoid whipsaw momentum trades and concentrate on company fundamentals to target strong, risk-adjusted returns.

Read more from Richard Colwell Less Bezzle, more sparkle in the UK!